The future of life and health insurance: How to stop ‘losing’ 40 million potential customers

Nov 23, 2015 | BLOG

Guest Blog: Future of Ageing 2015 series

By: Matt Singleton, Swiss Re

This photograph was taken three years ago and it’s one of my many favourites.

That adorable boy in the middle is my son who’s now four and recently started school. That adorable man on the left is my father who’s now 75. He’d only just retired at the time – very late in life for those of us not from the likes of Mexico, where many people work into their 70s.

The least adorable of this trio is the man on the right – that’s me. Historically, I’d have been the staple Life & Health insurance customer. I’m [said in a whisper] 40, I’ve now got two kids, a mortgage and I live in the so-called ‘developed world’.

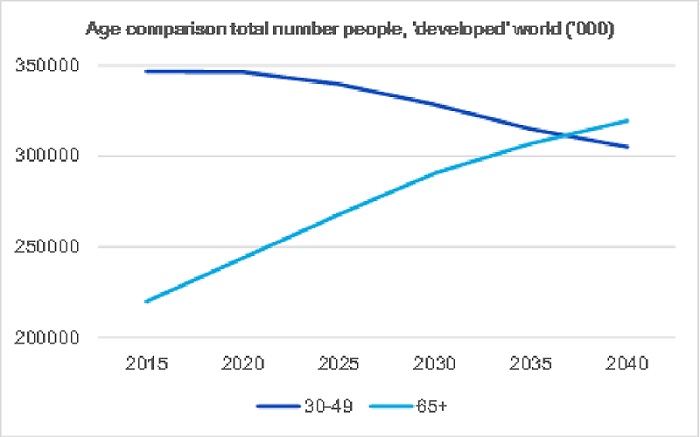

When considering ageing societies, we often talk about how quickly we’ll see the proportion of over 65s rise, but what’s happening to my current age group? Well, over the next 25 years we’ll see a dramatic decline in the population aged 30-49 in developed countries. Because of lower historic birth rates, we’ll ‘lose’ 40 million of the insurance industry’s supposed ‘ideal’ customers.

40 million! That’s pretty much the entire population of Argentina by the time I myself reach 65 and the young lad in the middle of the picture is just about 30. Or, to put it another way, we’re in the process of seeing our potential market reduced by the population of Estonia every single year. So what can we do?

The growing ageing population opens new doors and the exciting prospect of a completely new way of thinking. For every middle-aged person we ‘lose’, we gain 2.4 over 65s (see graph).

This means we must better serve the increasing number of people similar to the man on the left and help the likes of me prepare for when I reach my older age, which seems to be approaching quicker every day…

But this doesn’t come without obstacles … people’s key concerns continue into older age: what happens if I become sick or disabled? How will I be cared for and how will I pay? The issue for insurers is that the likelihood these risks will occur increases as people age. And the issue for customers is that the cost of insuring themselves against these risks also rises.

The insurance industry can adapt existing products and create new ones to provide real value for the expanding senior segment.

But this cannot happen without policies that provide a nurturing environment for new approaches. Regulation should support consumers in making the best decisions for their circumstances. If the consumer profile is changing, the insurance industry should move with them – as should regulation.

Looking at successes in other markets – like senior cancer cover in Asia or senior prescription supplemental medical plans in the US – is a good starting point. How can we improve regulatory environments to allow the ‘export’ of these valuable approaches to new markets?

Let’s not look at this as ‘losing’ the 40 million people that we could have helped, but instead look at how we can help the ‘new’ 100 million customers we stand to gain.

After all, I want to make sure that the boy in the middle of the photograph is cared for into his old age!

All figures are from the UN, 2012, medium fertility scenario.

Matt Singleton

Vice President and Senior Business Analyst, Swiss Re