Replacing the replacement rate: How much is ‘enough’ retirement income?

Oct 20, 2016 | BLOG

By: Dr Bonnie-Jeanne MacDonald, Dalhousie University

The final earnings replacement rate – where 70% is often advocated as the ‘right’ target – has been a longstanding and widespread measure of retirement income adequacy. Financial planners use this benchmark, as do actuaries and other pension plan advisers, academics, and public policy analysts

It underlies pension systems, drives research that determines whether populations are prepared or not prepared for retirement, and the backbone of retirement planning software.

But does it do the job that it is supposed to do? Will 70% of a worker’s final annual employment earnings sustain living standards after retirement?

The problem

After an extensive literature review, we determined that there is no clear demonstration that for a sufficient sample of workers who hit the prescribed target of 70%, living standards are, in fact, approximately maintained after retirement. We therefore decided to test it ourselves.

In MacDonald, Osberg and Moore (2016)1, we tested the conventional earnings replacement rate using one of the world’s largest dynamic micro-simulation models of society – Statistics Canada’s LifePaths dynamic population micro-simulation model. We asked whether those individuals from the 1951–58 Canadian birth cohort who attain roughly a 70% final employment earnings replacement rate at retirement actually achieve approximate continuity in their living standards.

We found that the conventional replacement rate is a poor metric of retirement income adequacy. Workers who hit this target were found to experience a wide range of living standards continuity after retirement, and we were unable to locate a ‘type’ of worker for whom the 70% target accurately predicts standard of living continuity.

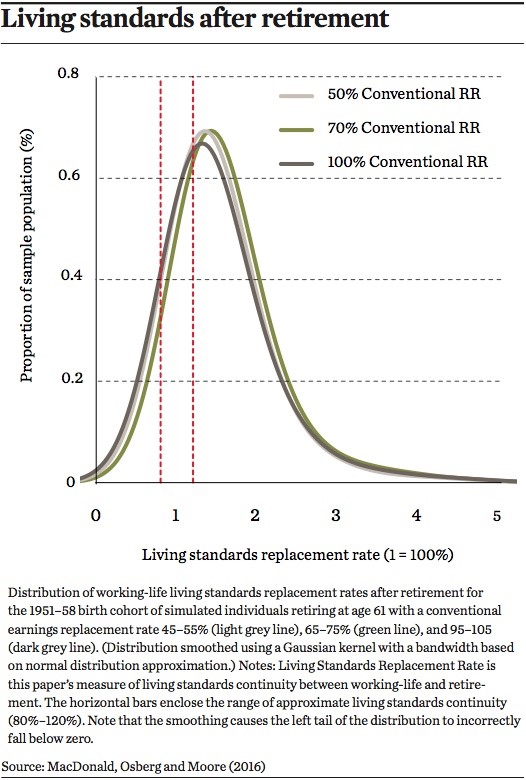

Regardless of whether we looked at workers who hit a 50% earnings replacement rate at retirement, or a 100% earnings replacement rate, the distribution of living standards continuity into retirement looked nearly identical (see figure). In fact, we found that the correlation between a worker’s earnings replacement rate and living standards continuity after retirement is only 11%, making it an unreliable benchmark for retirement income adequacy.

The issue is not whether 70% is too high or too low. The earnings replacement rate fails because a single year’s employment earnings are not a reliable representation of a worker’s living standard – it relies on an inadequate measurement period (only one year), does not incorporate important components of consumption sources (such as home equity), and ignores household size (particularly children). These omissions are crucial in calculating living standards. Moreover, these omissions interact, and the effect of improving one may not emerge without the others. Indeed, it is primarily owing to these significant and interacting omissions in the earnings replacement rate formula that there has been such a wide range of (often conflicting) reports on the retirement preparedness of populations and pension system reform impacts.

The solution

After concluding that the conventional earnings replacement rate is not fit for purpose, I developed the Livings Standards Replacement Rate (LSRR).

Drawing from best academic practices, the LSRR determines how well a worker’s living standards will be maintained after retirement by comparing how much money a worker has available to support their personal consumption of goods and services before and after retirement.

Analysts invest time and effort in the study of retirement income adequacy, but an unreliable benchmark for ‘adequacy’ can lead to misleading conclusions. The LSRR offers a real alternative to the conventional replacement rate, and is bridging the gap between good science and industry need.

The LSRR calculation considers the entire family, includes consumption components comprehensively and covers a representative number of years. Having this framework available for analysts to reference will enable a more consistent measure of retirement income adequacy, so as to facilitate the interpretation, comparison and integration of findings across different analysis (between authors, over time and across nations). This would help the study of retirement income adequacy to move forward.

The LSRR provides an accurate, understandable, and consistent measure of retirement income adequacy, and this concept has proved extremely useful to practitioners in serving their clients². It has also been applauded for its academic merit (having won the 30th International Congress of Actuaries’ Pension, Benefits and Social Security Scientific Committee Award Prize for Best Paper in 2014). It has also been published in a significant peer-reviewed academic journal, which can be downloaded without fee: https://dx.doi.org/10.1017/asb.2016.20.

Population ageing has led to widespread concern regarding retirement income adequacy, and now is time to adopt a better measure. The LSRR has penetrated the Canadian financial industry, and has gained considerable traction internationally. If the LSRR can create the necessary paradigm-shift within the pension industry and study of retirement income adequacy, the benefit to the public is incalculable.

Dr Bonnie-Jeanne MacDonald

Dalhousie University

Andrew Rear spoke at the ILC-UK event Europe’s Ageing Demography, at the European Economic and Social Committee in Brussels, on the 5th November 2014. This is the second in a series of guest blogs by Andrew which will expand upon the key issues he raised in Brussels