By: David Sinclair, Ben Franklin, Cesira Urzi Brancati

For good reasons, young people have been the focus of the majority of initiatives aimed at increasing financial capability. Younger people have historically had lower understanding of financial issues than older people and there is quite rightly, a recognition of the value of starting young with basic numeracy skills.

Older people are perceived to be better at “living within their means” and when older people do borrow, they do so “responsibly”. This contrasts with images of younger people, who are often seen as financially irresponsible and are characterised as being saddled with debt.

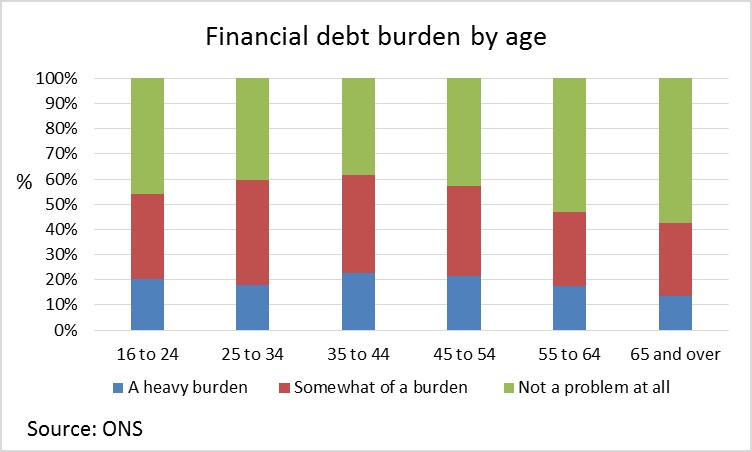

As ever the picture is far more nuanced than the prevailing stereotypes might suggest. While the 25-34 age group faces the greatest burden from mortgage debt, the 35-44 age group faces the greatest burden from non-mortgage debt (i.e. credit cards, loans and overdrafts). The over 65s are not immune from these challenges – nearly 14% of this age group report a heavy burden from non-mortgage debt, and 7.5% from mortgage debt.

Following the launch of the Money Advice Service led Financial Capability Strategy, ILC-UK have joined the “Older People in Retirement Steering Group” to feed our views into the process over the next three years. This blog represents our initial thoughts on the need for action. In October 2015, we presented these thoughts to a group of senior global finance ministries at an OECD event in Malaysia.

The need for financial education among older people is arguably higher than ever. We set out below 7 reasons why we believe there is an urgent need to better understand financial capability and its impact on retirement.

1) More (diverse) older people means more diverse needs

A growing number of older people means increasing diversity in people’s retirement realities. More older people have accumulated financial and property wealth on entering retirement and require advice on how they might use these assets to fund retirement. Yet at the same time, 1.6 million people remain below the poverty line and may require more advice on managing their money as well as their debts. Rising incidences of divorce in later life can result in people facing income shocks in retirement forcing them to make financial decisions they may not have originally planned for. With increasing longevity, dementia becomes more likely and managing money potentially more difficult.

2) The move towards digital banking and payments makes things a bit more complex

Whilst digital banking has the potential to help people better manage their money in real time, there are some short term challenges in an ageing society. Many, including but not exclusively, the most financially excluded, have found that managing money in “jam jars” was the best way to keep a track of their incoming and outgoing expenditure. However, for older people who aren’t online, keeping track is potentially more difficult. Whereas in the past local bank branches may have supported the needs of older people, the number of branches has been in steep decline – in 1988 there were over 20,000 bank branches but by 2012 this had fallen to less than 9,000. Work is still needed to increase trust of online payments by older people and to improve overall internet access for older people.

3) Liberalisation and individualisation puts responsibility and risk onto individuals

The Government’s announcement that older people will no longer be effectively forced to annuitise their pension pots was broadly welcomed. Yet it will require a more engaged older population who will have to actively decide how to manage their income throughout retirement.

ILC-UK research found that of those aged over 55 with a private pension but not yet retired, only half understood what an annuity was “quite or very well”. Income drawdown was even less well understood.

The decision as to what to do with pension pots will no longer be a one-off decision made at the point of retirement. Instead people are likely to be altering and adapting their financial planning strategies throughout retirement including well into later life.

In this environment, low levels of financial capability may lead consumers into buying products they do not need or understand, or that fail to meet their long-run consumption needs, causing them harm.

4) More older people have experience of debt

Problem debt remains a greater challenge for younger than older people. But over the next decade or so, more older people are likely to find themselves with experience of problem debt. Yet, across all ages, people don’t access the support available. ILC-UK analysis of the Wealth and Assets Survey shows that among consumers who felt burdened by debt (approximately 17% of the sample), only about 1 in 8 (or 12.7%) received any advice at all to help them deal with their debts, and among them, 3 in 5 received advice from a free agency

5) Professionalization of money advice could reduce access

Greater professionalization and regulation of advice is important if we are to protect consumers. However in the short term, initiatives such as the Retail Distribution review have arguably reduced access to financial advice (although financial advice has of course always been the preserve of the few). Employers could offer more by the way of advice but many are quite rightly, fearful of doing so. Individuals will need to be better prepared to ask the right questions of the financial services industry, particularly as new models of mass advice (e.g. robo advice) begin to appear.

Consumers are aware of increasing choice in the world of financial products and services, but they are increasingly distrusting of intermediaries who they may once have used to navigate this world, and are able to use the internet for purchasing financial products and services. However, with low levels of financial capability, consumers are not well equipped to go it alone. The recent “pension freedoms” has brought this debate to the fore.

6) Greater recognition of the value of older consumers

The increasing recognition of the value of older consumers is positive. But it may make this group a target for both genuine marketing as well as for scams and elder abuse. Preparing older people to be savvy consumers will be increasingly important.

7) Education levels of older people are lower than young

Older people tend to have lower formal educational qualifications than young. This isn’t necessarily an indicator of financial capability but it is worth reflecting that cuts to adult learning may be unhelpful in terms of our desire to increase financial capability.

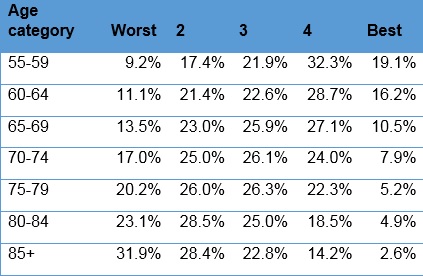

ILC-UK analysis of the English Longitudinal Study of Ageing highlights how levels of financial literacy/numeracy are lowest among those in the oldest age groups. (1)

Numeracy/financial literacy scores

What does all this mean?

It is clear that we need to know more about how to deliver financial education in old age. We also need to know whether it actually works. Work done in this area so far (including by Age UK) suggests there are four key issues which need to be considered in terms of this target audience. There remains a need for greater evaluation (see below) but more needs to be done in the following areas:

- We need to recognise “where people are”. Life events are an important trigger for new or different financial products and services and can therefore be a good place to target financial capability interventions.

- Face to face support is important

- Initiatives should explore how we can first define and subsequently target the most at need groups.

- Initiatives must consider the broader context of older people’s community engagement. An age friendly community is necessary if we are to properly engage older people.

What needs to be done now? (arguably these apply to all ages)

Poor levels of financial capability are compounded by inertia in the face of seemingly complex problems which means many people do not make active financial decisions even when it would be to their benefit (i.e. switching bank accounts or insurance providers).

Government, with providers, need to develop practices which work with the behavioural biases of consumers so as to help nudge them into “good” decision making, and where this isn’t possible, good default options are needed to avoid the worst outcomes.

Clearly we need to improve levels of financial capability if that is possible but this is a task that may take a generation or more. For this reason we also need some low risk/default/safe options. We must try and simplify finances for all of us. It doesn’t benefit us that financial services have become so complex.

It is vital that we evaluate the impact of financial capability interventions. Evaluation must be much better than in the past and must help us answer the question of “what is the best way to spend the marginal pound”. We might need to ask whether raising financial capability is achievable and leads to better outcomes than say initiatives that limit the number and complexity of available products or that seek to nudge consumers into making certain decisions.

The extent to which financial education is effective in raising financial capability is much debated. In part, this is because financial capability, broadly defined, is not just about knowledge of things like APR or compound interest but about behavioural traits such as preferring short term rewards over long term gains and potential overconfidence or inertia in the face of complexity. Financial education may therefore be part of a solution at the margin, but it is by no means a silver bullet.

There is a value in exploring how and whether generalist advisors can better provide basic money advice. And finally, we must ensure that the policy drive for increasing quality standards doesn’t prevent innovation.

A mass market advice offering is essential. Technology is such that other industries are able to provide a degree of tailored advice on the basis of information that has been inputted by an individual – i.e. NHS Direct symptom checker. And some parts of the pensions industry have also started developing online tools to help their customers understand what their investment choices might mean for their future. But nothing exists for the everyday consumer with modest wealth to invest. This must change.

And finally, digital exclusion is a significant barrier to capability and we must continue to tackle the challenge.

In conclusion

The world of money is becoming more complex and older people are more diverse in their experience and needs. Some older people need help understanding how to manage money. Others may need support with investments. Our analyisis of ELSA (50+) highlights how the oldest among their sample have the lowest level of numeracy. With more and more older people reaching their 80s and 90s we need to find a way to ensure that we don’t see a growing number of people struggling with money management. There is undoubtedly a need to raise financial capability levels across the whole lifecourse but given this evidence we believe that financial capability initiatives must ensure that the oldest old get the support they need.

Notes

1) Financial literacy scores

This variable puts individuals into groups according to numerical ability. There are 5 groups

These are the questions (FYI)

q1) If you buy a drink for 85 pence and pay with a one pound coin, how much change should you get?

q2) In a sale, a shop is selling all items at half price. Before the sale a sofa costs £300. How much will it cost in the sale?

q3) If the chance of getting a disease is 10 per cent, how many people out of 1,000 would be expect to get the disease?

q4) A second hand car dealer is selling a car for £6,000. This is two-thirds of what it cost new. How much did the car cost new?

q5) If 5 people all have the winning numbers in the lottery and the prize is £2 million, how much will each of them get?

q6) Let’s say you have £200 in a savings account. The account earns ten per cent interest per year. How much will you have in the account at the end of two years?

David Sinclair, Ben Franklin, Cesira Urzi Brancati

ILC